Over the last two years, nothing has upended marketing budgets more drastically than the roll-out of iOS14 and the subsequent downstream impact on performance across mobile advertising.

Now that we are one year in, many of these initial drastic spend shifts have normalized (return of FB budgets), while other new channels have become a growing part of the marketing mix (hello TikTok).

At Rockerbox, we’ve had a front seat to the evolving marketing mix of DTC and e-commerce companies, as hundreds of them leverage our SaaS platform to holistically measure their marketing performance.

With that being said, below we’ve compiled some initial trends we’ve seen evolve over the last year.

And of course here for our automatically updating dashboard on WoW share of spend across vendors.

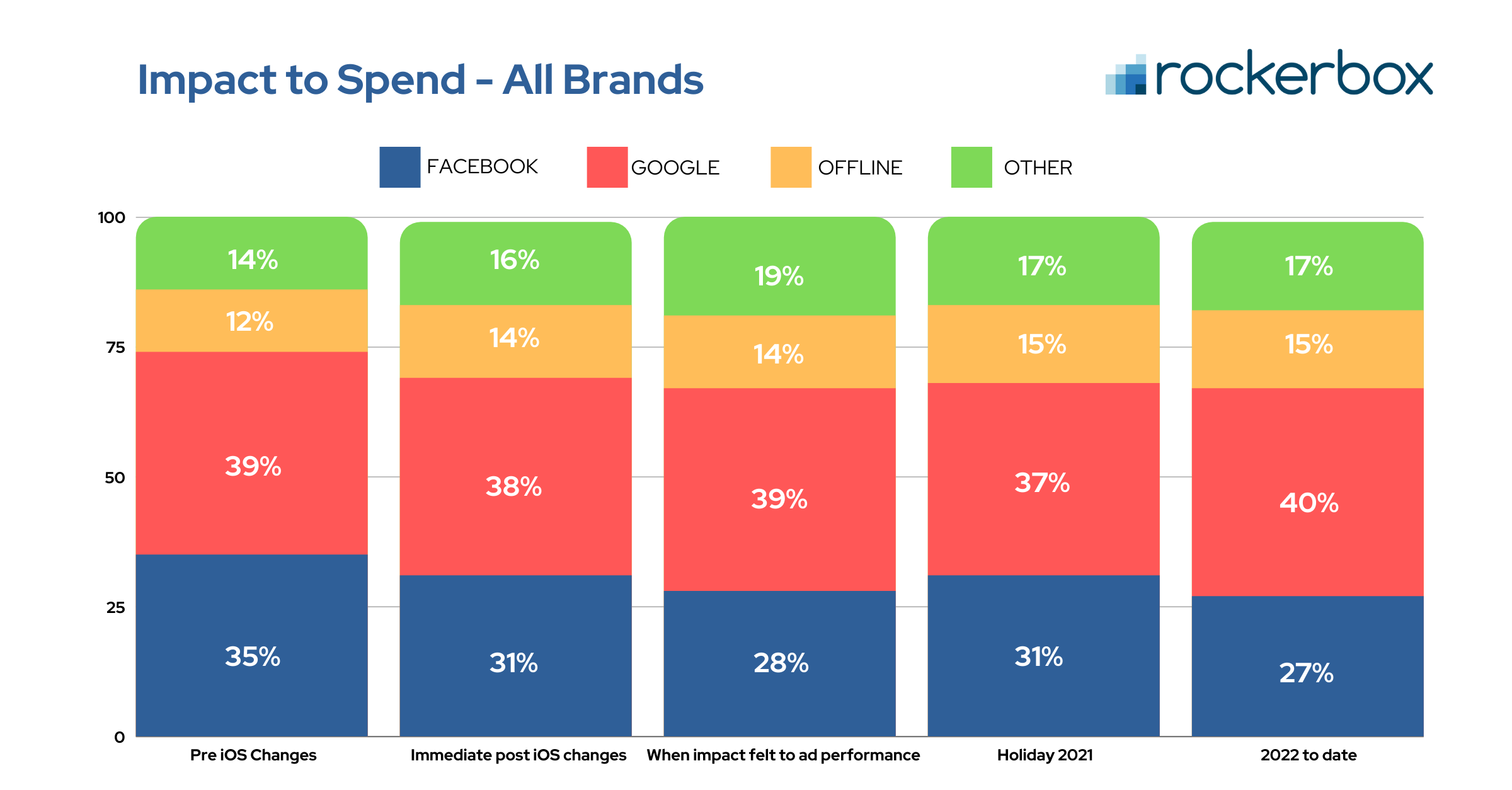

Overall Trends

1The biggest winners of iOS changes remain the channels that have been able to hold spend even after the recent spend shifts in mid-2021

Google

For small brands, spend allocation increased from 25% to 39% from Jan 2021 to 2022.

TikTok

At the start of 2021, most brands were barely testing, with budgets under .25% of total spend. TikTok spend has climbed upwards of 2% of total spend into 2022.

Offline Channels- Direct Mail, Linear TV, and OTT / Streaming TV

For large brands, spend against offline channels increased to upwards of 20% of spend in 2022, up from 13% at the start of 2021

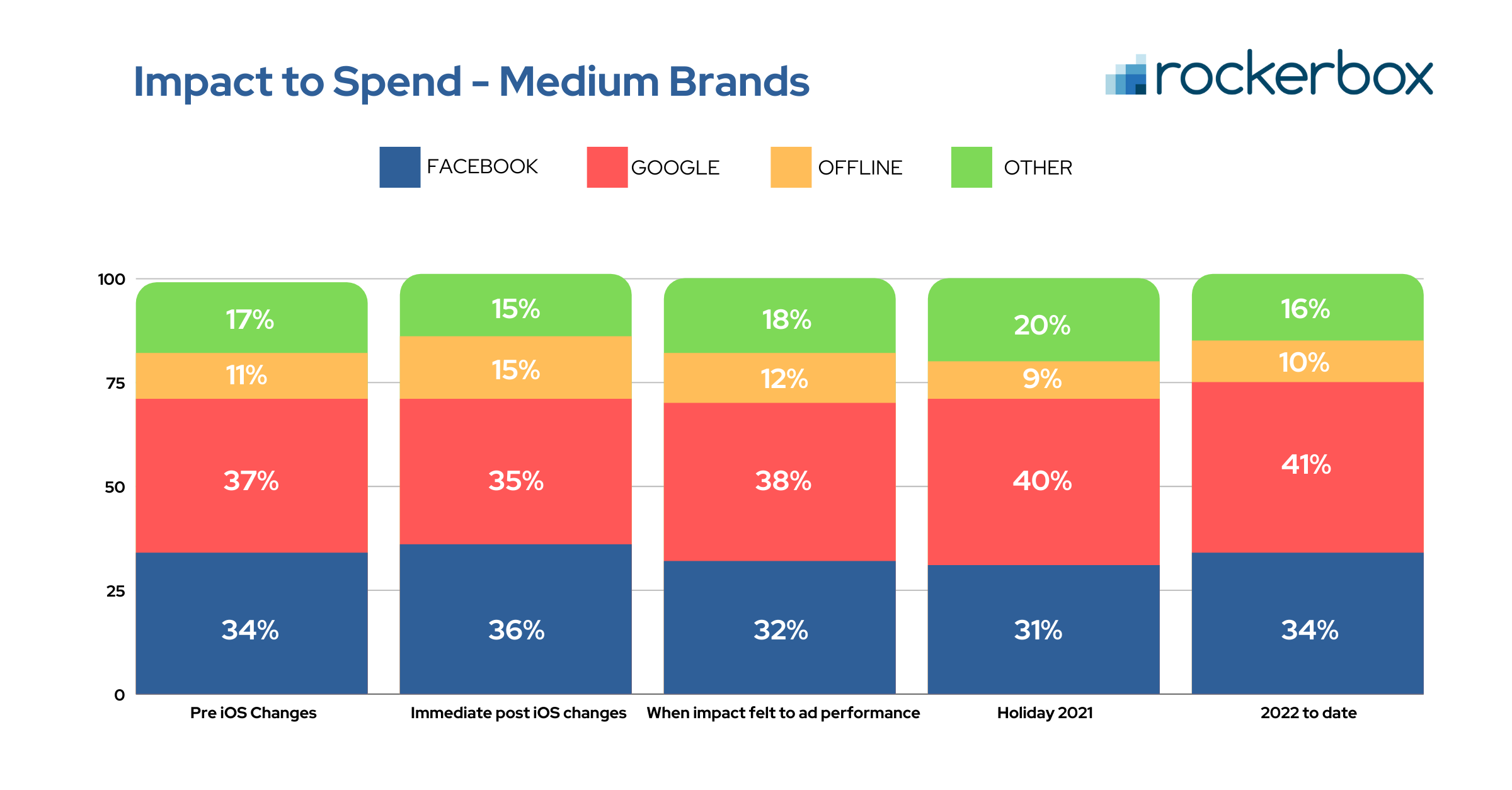

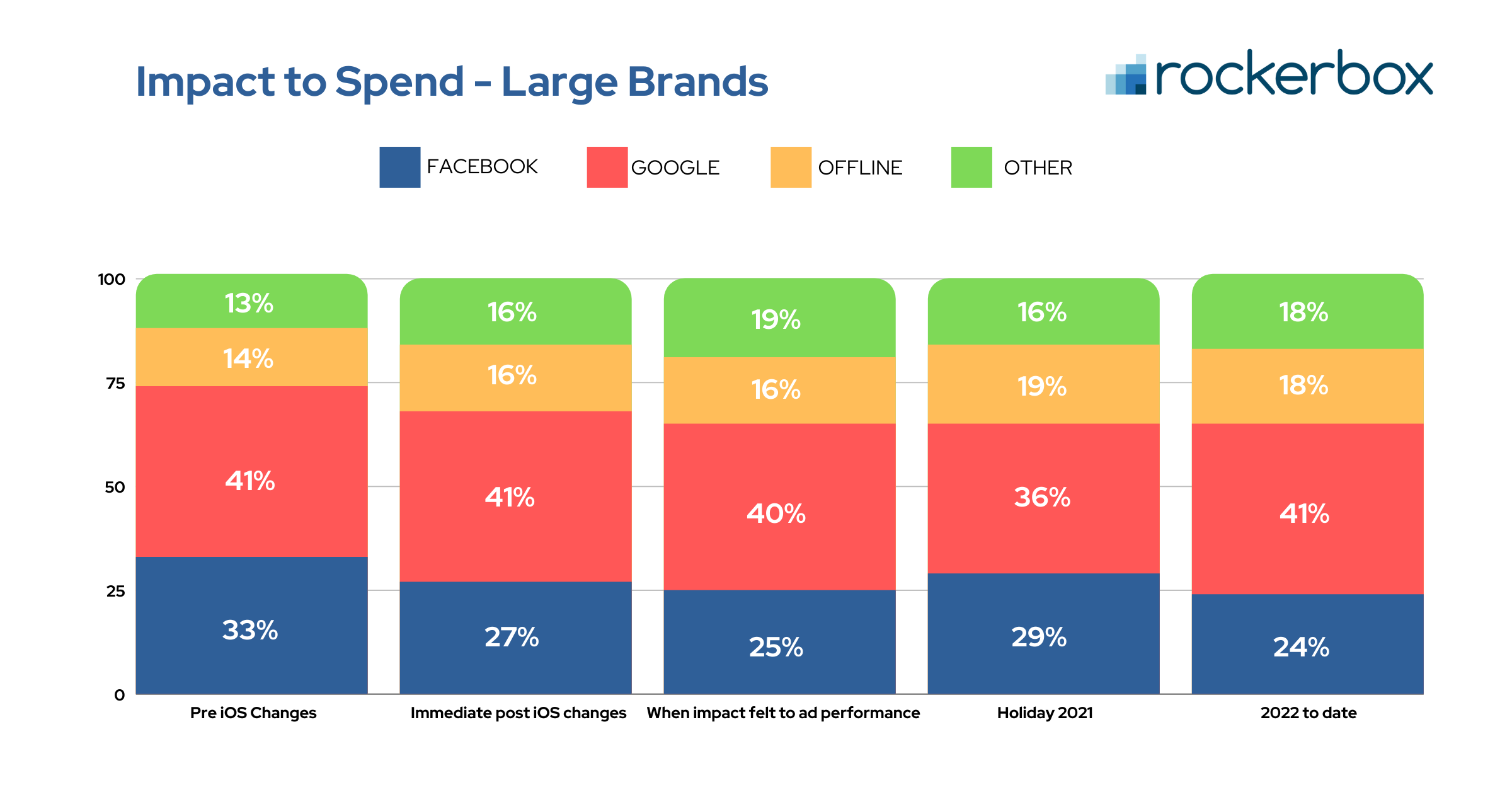

2Channel marketing mix over the last year is largely driven based on the size of the brand

Small brands were the hardest impacted by the drop in FB performance and the fastest to pull spend, yet that spend has recently returned in 2022.

The adverse impact small brands felt was a result of having the largest % of the budget on FB via broad audience targeting, leaving them over-exposed. This spend shifted to Google as the brands were under-invested in non-branded search and shopping.

Larger brands had a more diversified marketing mix pre-iOS changes were not heavily reliant on FB, and instead were spending across offline channels (Direct Mail, OTT, Linear TV).

When FB performance suffered, they already had proven non-mobile channels to shift spend into 2022, spend into offline channels held, not returning to FB, unlike smaller brands

For Small Brands

(sub $1.5M/month in revenue, spending under $500k/month, mainly run digital channels FB and Google)

Facebook has made a resurgence, with brands shifting spend back to Facebook over 2022, despite being most adversely impacted by iOS14 changes to Facebook performance in 2021

Big hit to Facebook performance as a result of brands being over-exposed and over-leveraged on Facebook, with upwards of 50% of their spend on Facebook.

During 2021, smaller brands doubled down and focused on scaling non-branded shopping and search.

For Large Brands

(Over $20M/month in revenue, spending over $2M/month, with a scaled and diversified marketing mix, running digital and offline channels.)

Brands immediately shifted greater spend into offline channels or began testing these channels if they weren’t already running them. Typical on-ramp started with Direct Mail and OTT, then scaling into Linear TV.

Offline channels’ biggest advantage remains the ability to instantly scale spend. And for rapidly growing DTC brands, few things matter more than performance at scale

In follow-up posts, we’ll cover in detail the shifts in performance within each channel across brand sizes, calling out actionable next steps and recommended opportunities to test to continue to evolve your marketing mix.

Google

Google Facebook

Facebook Instagram

Instagram TikTok

TikTok Snapchat

Snapchat Reddit

Reddit Pinterest

Pinterest

.png?width=50&height=56&name=medal%20(1).png)

.jpg?width=70&name=Sara%20Livingston-headshot%20(2).jpg)